Decisions taken regarding the approach to funding will therefore determine the rate or pace at which this advance provision is made. Although the Scheme Regulations specify the fundamental principles on which funding contributions should be assessed, implementation of the funding strategy is the responsibility of NILGOSC, acting on the professional advice provided by the Fund Actuary.

Funding strategy statement

NILGOSC has prepared a Funding Strategy Statement in accordance with Regulation 64 of the Local Government Pension Scheme Regulations (Northern Ireland) 2014.

The purpose of the statement is to:

- establish a clear and transparent fund-specific strategy which will establish how employers’ pension liabilities are best met going forward;

- support the desirability of maintaining as nearly constant employer contribution rates as possible;

- ensure that the regulatory requirements to set contributions to ensure that the solvency and long-term cost efficiency of the fund are met; and

- set out a prudent longer-term view of funding those liabilities.

Access our Funding Strategy Statement.

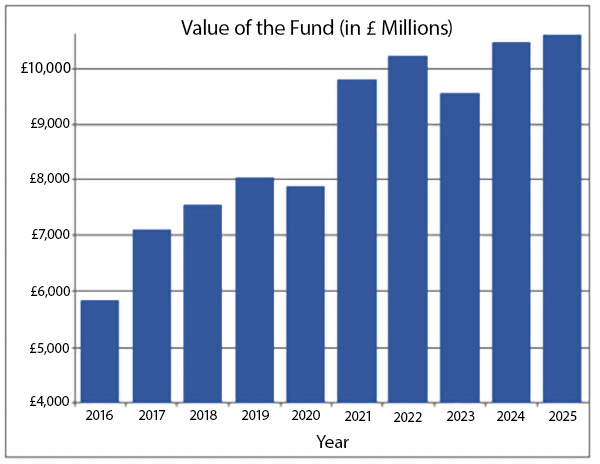

Fund value

The value of the Fund at 31 March 2025 has increased by £489m to £10.952bn (2024/25 £10.463bn) or 4.67% on the previous year.

Market values can fluctuate widely over short periods of time, reflecting short-term changes in investment conditions. In contrast, the triennial valuation of the fund is concerned with the long-term and uses actuarial assumptions.

Actuarial Valuation

The assets and liabilities of the Fund are valued every three years by the Scheme Actuary. Following each valuation, the Actuary certifies the employers’ contribution rates to maintain the viability of the Fund. The latest Valuation Reports and Statements are available in the ‘Document Library’ section under ‘Valuation Reports’.