The 12-month period to 31 March 2025 was characterised by significant market fluctuations, driven by central bank actions, geopolitical developments and inflationary concerns. Despite material volatility, developed equities delivered positive performance, with regional disparities influenced by political and economic factors. Fixed income markets benefitted from rate cuts early in the year but faced headwinds later as inflation concerns persisted. Gilt yields saw notable volatility, reflecting shifts in monetary and fiscal policy, as well as external influences like US Treasury movements. These dynamics underscored the challenges of navigating markets during a period of heightened uncertainty.

The People’s Bank of China (PBoC) was the first major central bank to begin the rate cutting cycle in 2024, reducing rates by 10bps in February. The European Central Bank (ECB), Bank of England (BoE) and US Federal Reserve (Fed) later followed suit. The ECB cut interest rates by 100bps over the year. The Bank of England cut interest rates three times, 25bps each time, taking the base rate to 4.5% at year-end. The Fed were the last to implement rate cuts, with a 50bps cut in September 2024, followed by a further 50bps cut over November and December.

The dollar strengthened at the start of the year to 31 March 2025 amid expectations that other major central banks would cut interest rates ahead of them, coupled with the receipt of strong US economic data from Q4 2023. Despite fluctuations throughout the year, the dollar ended Q4 2024 ahead of the euro, sterling and yen. This was again driven by a stronger economic outlook for the US and revised interest rate cut expectations. Sterling suffered throughout the year as the economy remained in a technical recession at the start of the year and inflation remained elevated.

Equities

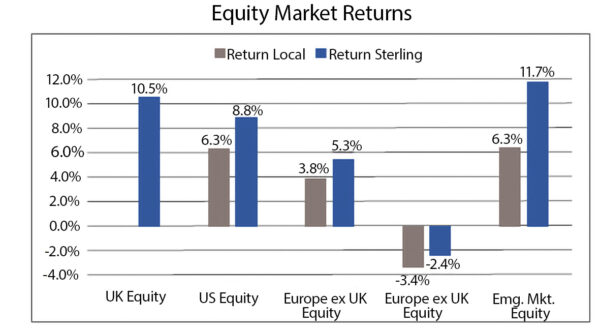

Equity markets experienced considerable volatility over the 12-month period, shaped by evolving global economic and political developments, but delivered positive returns over the period. Global markets rallied over the second and third quarters of 2024 as central banks began the rate-cutting cycle, easing recessionary fears and supporting risk-on sentiment. However, weaker-than-expected US employment data and an unexpected interest rate rise in Japan led to heightened volatility in late July and early August. Markets recovered in September 2024, following central bank interventions and the announcement of Chinese stimulus measures. While Trump’s presidential election victory in November 2024 initially bolstered global equity markets, as his business-friendly policies increased optimism around higher growth, tax cuts, and deregulation in the US, trade tension and tariff threats proposed by Trump subsequently drove significant headwinds for US equities over Q1 2025. The emergence of the Chinese AI firm DeepSeek, which posed a competitive threat to US technology firms, also weighed heavily on the region overall. Conversely, UK and European equities performed well over the latter period of Q1 2025, as investors rotated into financials, defence, and energy sectors and away from the US given the uncertainty surrounding trade tariffs.

US equities delivered strong performance over 2024, driven by easing inflation data and the long-awaited interest rate cuts. In particular, the region benefitted from the strong positive returns of Nvidia which accounted for 30% of total gains recorded by the S&P 500 as at 30 June 2024, alongside a concentrated set of technology stocks. Despite sustained positive performance throughout the year, US equities experienced a sell off towards the end of December as uncertainties surrounding President Trump’s proposed policies began to grow and a further reduction towards the end of March 2025 as investor sentiment reflected imposed US tariffs.

European equities were positive over the year but underperformed the wider globe due to relative economic weakness and the backdrop of political uncertainty in France and Germany, which both held parliamentary elections in 2024.

With UK equities having suffered at the beginning of 2024 due to the UK entering a technical recession in December 2023, there was a rebound in performance over Q2 2024 driven primarily by improving inflation data and GDP growth and the region delivered positive returns on an absolute basis over the 12-month period.

There was a slight reversal over Q4, due to the wider equity market sell off in December and a weaker economic outlook for the region, with the BoE deciding to hold interest rates constant at their meeting in December and UK inflation rising over November.

Japanese equities delivered negative returns on an absolute basis over the year period, significantly underperforming other regions over Q3 following an unanticipated interest rate rise by The Bank of Japan (BoJ) in July. Performance recovered slightly over Q4 as the BoJ kept rates constant amid a recovery in annual inflation data for November.

Within emerging market equities, Taiwan emerged as the strongest performer for the year, benefitting from the increased demand in semi-conductors within AI. Emerging market equities suffered significantly over Q4 as a result of the US election, given the aggressive trade policies proposed by President Trump, but posted overall positive returns on an absolute basis over the year. Returns since NILGOSC’s investment in November 2024 were however negative.

The Fund’s passive investment in the LGIM Low Carbon Transition Fund (LGIM LCT) delivered positive returns over the year in line with the wider market benchmark, driven primarily by its concentrated allocation to a select number of Technology stocks. Growth-focused mandates outperformed value-oriented strategies over the 12-month period, as the sustained equity market expansion during the first three quarters of the period created more favourable conditions for growth strategies.

UK Fixed Income

Fixed income markets experienced varied performance across the credit spectrum over the year, driven by ongoing uncertainty surrounding central bank rhetoric, inflationary pressures, and economic expectations.

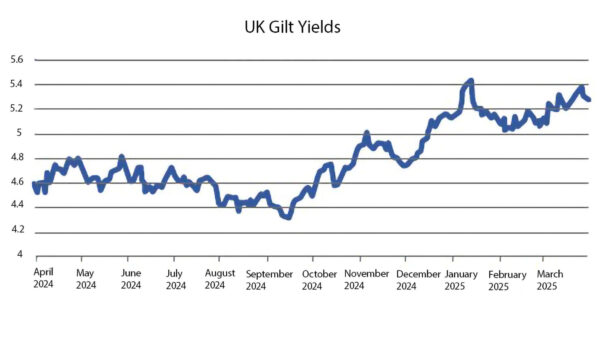

Overall, UK fixed and inflation-linked government bonds fell in value over the year. UK gilt yields fluctuated significantly over the 12-month period, driven by central bank policy changes, fiscal developments, and external geopolitical factors. Gilt yields rose initially at the beginning of the period as the Bank of England opted to keep the base rate constant at 5.25%. Gilt yields subsequently began to fall as the BoE cut interest rates to 5% in August 2024 and amid increased investor optimism for the UK economy following the appointment of the new Labour government. A sharp rise in yields then followed the October 2024 Budget, which projected higher borrowing and further raised inflationary concerns. This rise continued as investors priced in fewer rate cuts for 2025.

Gilt yields continued to rise over Q1 2025, largely in tandem with US Treasury yields, which spiked in response to Trump’s economic policies. However, the yield rise moderated later in the quarter, with the Bank of England cutting rates by 0.25% to 4.5% in February, before holding them steady in March.

UK credit performed positively over the period despite rising underlying yields, as credit spreads tightened against the backdrop of easing inflation and monetary policy. High Yield Credit outperformed Investment Grade given its lower sensitivity to changes in yields.

Global Fixed Income

Global fixed income markets were highly reactive to changing interest rate expectations across the globe. As the rate-cutting cycle began in Q3 2024, this created a risk-on sentiment which drove the tightening of credit spreads. Against this backdrop, investment-grade credit outperformed high-yield credit, due to greater sensitivity to falling yields. However, by Q4 2024, fixed income markets struggled as inflationary concerns reduced the number and extent of expected interest rate cuts forecasted for 2025. As a result, High Yield credit outperformed, benefiting from tighter credit spreads and lower sensitivity to yields. As central banks began the rate cutting cycle over Q3 2024, investment grade credit performed well as spreads tightened further. Moving into 2025, there were marginal positive returns for corporate fixed income markets, though bonds with greater interest rate sensitivity underperformed as investors again began to price in fewer interest rate cuts through the year. Central bank rhetoric played a key role in market sentiment, with indications of slower rate cuts in 2025 weighing on valuations but supporting higher-quality credit market.

Property

The UK property market faced persistent challenges over the year to 31 March 2025, particularly within commercial real estate, driven primarily by higher borrowing costs. The UK real estate market showed signs of stabilisation over Q2 and Q3 2024, as the pace of capital value declines began to slow. This trend continued throughout the remainder of the year as political and economic certainty improved. By Q4 2024, the UK real estate market had stabilised; capital value declines had moderated, competition within the market strengthened and income returns across sectors remaining robust. Total returns over the 12-month period across residential, industrial and hospitality were all positive.

Whereas, the office space sector continues to struggle, primarily driven by a reduced demand for office space not in “prime” locations.

Global property markets reflected varying regional and economic conditions and sector-specific trends. Some regions benefited from post-pandemic recovery momentum and strong demand for industrial and logistics assets, others faced headwinds from rising interest rates, inflationary pressures, and shifts in office space demand due to hybrid working models. Retail properties continued to face challenges, particularly in markets where consumer spending remained subdued, while residential property markets demonstrated resilience in regions with strong population growth and housing shortages.

Infrastructure

The outlook for the infrastructure market at the start of the period highlighted cautious optimism as moderating inflation and stabilising interest rates eased pressure on valuations. Resilient transport volumes, steady regulated earnings, and growing demand for power-intensive AI applications bolstered returns over the 12-month period.

This materialised over Q3 2024, as infrastructure benefitted from falling inflation and the beginning of the rate cutting cycle. Interest rate cuts particularly benefitted long-dated infrastructure assets and allowed for a rebound in listed rate-sensitive sectors such as utilities. Transport and utilities later benefitted from increased government spending, particularly under Labour’s economic policies, which highlighted energy and public infrastructure improvements. In the private sector, investment into transport, broadband, and clean energy remained strong, though increased borrowing costs weighed on valuations.

The graphs below highlight the UK Gilt Yields and the Equity Market Returns of the main asset classes/regions for the year to 31 March 2025. These Returns are shown in local currency and Sterling terms.